Info Home - hledger

hledger is friendly, fast, and dependable accounting software for tracking money, investments, cryptocurrencies, time, or any countable commodity. It uses human-readable plain text data

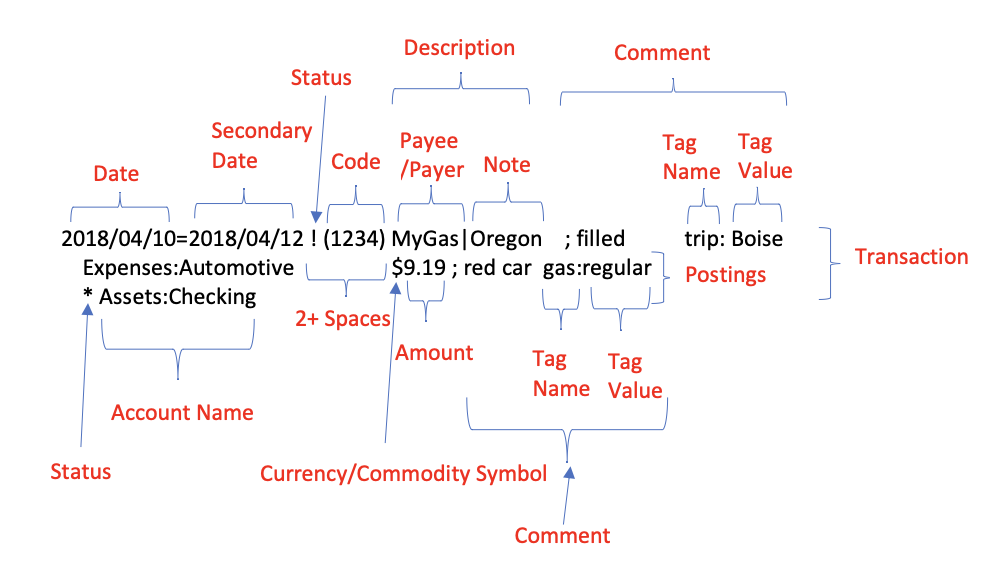

hledger manual (1.51) » Journal

hledger’s usual data source is a plain text file containing journal entries in hledger journal format.

1 2 3 4 brew install hledger hledger --version

Journal Account Type hledger knows that in accounting there are three main account types:

Account Type Note AssetAthings you own LiabilityLthings you owe EquityEowner’s investment, balances the two above

and two more representing changes in these:

Account Type Note RevenueRinflows (also known as Income) ExpenseXoutflows

hledger also uses a couple of subtypes:

Account Type Note CashCliquid assets ConversionVcommodity conversions equity

Transaction 一图流 Hledger Transaction 图片来自:(Almost) everything you wanted to know about hledger transactions – A User’s view of Hledger

基本使用 bal / balance A flexible, general purpose “summing” report that shows accounts with some kind of numeric data.

例行核对。检查每笔 transition 以及 balance assertions 。

1 hledger bal [-f xxx.journal]

reg / register Show postings and their running total.

如果某个账户余额核对出错,可以列出其相关交易以便排查:

1 hledger reg [-f xxx.journal] -I 'Assets:Online:WeChat$' cur:CNY

check Check for various kinds of errors in your data.

检查 transactions 是按日期有序排列的:

1 hledger check ordereddates [-f xxx.journal]

areg / aregister Show the transactions and running balances in one account, with each transaction on one line.

aregister is best when reconciling real-world asset/liability accountsregister is best when reviewing individual revenues/expenses. 用接近于银行流水单的形式,列出某个账户的交易和 running balances 历史:

1 hledger areg [-f xxx.journal] 'Assets:Checking:ICBC'

好像 不能 像 register 那样通过 $ exclude sub-accounts —— 可以,再加一个参数用作 query:

1 hledger areg [-f xxx.journal] 'Assets:Checking:ICBC' 'Assets:Checking:ICBC$'

print Show full journal entries, representing transactions.

打印 transactions,补全空缺的金额:

1 hledger print [-f xxx.journal] -x 'Assets:XXX'

accounts 列出未声明的账户:

1 hledger accounts --undeclared

commodities 列出未声明的币种:

1 hledger commodities --undeclared

bs / balancesheet Show the end balances in asset and liability accounts.

看资产和负债汇总:

1 2 hledger bs cur:CNY hledger bs --cost

is / incomestatement Show revenue inflows and expense outflows during the report period.

看收入和支出汇总:

更新注意 1.50 - Transaction Balancing Transaction balancing is now done in a more robust way, using local precisions only (like Ledger) #2402 . Until now, a transaction was required to balance using its commodities’s global display precisions. Small imbalances were tolerated by configuring display precisions for the whole journal (with commodity directives).

比如这条 transaction 在 1.50+ 就不行:

1 2 3 4 5 6 7 8 9 339 | 2013-01-30 计算持仓均价 | Assets:Investment:Silver 600 XAGg @ 6.2454167 CNY | Assets:Investment:Silver -100 XAGg @ 6.2175 CNY | Assets:Investment:Silver -500 XAGg @ 6.251 CNY This transaction is unbalanced. The real postings' sum should be 0 but is: 0.0000200 CNY Note, hledger <1.50 accepted this entry because of the global display precision, but hledger 1.50+ checks more strictly, using the entry's local precision.

因为后两条的总额相当于 37.4725 CNY,除以 6 无法除尽,@ 6.2454167 CNY 无论保留多少位都没办法。

对于这种场景,直接不做这种均价化的处理了(至少不在除不尽的时候做),缺点是要自己管理「先入先出」。

另一种情况:

1 2 3 4 5 6 7 8 292 | 2024-02-01 饮料 | Expenses:Catering:Drink 380 JPY @ 0.049572 CNY | Liabilities:Credit:ICBC -2.6 USD @ 7.2451 CNY This multi-commodity transaction is unbalanced. The real postings' sum should be 0 but is: 0.000100 CNY Note, hledger <1.50 accepted this entry because of the global display precision, but hledger 1.50+ checks more strictly, using the entry's local precision.

这里的误差就没法避免了,因为银行在记账的时候做了舍入处理。考虑引入特殊的 account 来 absorb the imbalance:

1 2 3 4 2024-02-01 饮料 Expenses:Catering:Drink 380 JPY @ 0.049572 CNY Liabilities:Credit:ICBC -2.6 USD @ 7.2451 CNY Expenses:Adjustments:Rounding -0.0001 CNY

如果前两行的 @ UNITPRICE 都没有问题,也可以省略 Expenses:Adjustments:Rounding 的金额,让 hledger 自动计算。

或者使用 @@ TOTALPRICE 语法,避开除不尽的 @ UNITPRICE:

1 2 3 2024-02-01 饮料 Expenses:Catering:Drink 380 JPY @@ 18.83726 CNY Liabilities:Credit:ICBC -2.6 USD @ 7.2451 CNY

实践 按年拆分 Journal 一年一个 Journal 文件,日常只处理当年的文件,需要的时候可以把连续若干年的文件「连」起来一并处理。

用 hledger close 命令生成 closing 文件和 opening 文件。

设起始年是 2000 年,记录于 2000.journal 文件。在 2000 年结束后,运行:

1 2 3 4 5 6 7 8 9 hledger close -f 2000.journal \ --close --show-costs \ -e 2001 --close-acct Equity:OpeningClosing:2001 \ Assets Liabilities > export /2000-closing.journal hledger close -f 2000.journal \ --open --show-costs \ -e 2001 --close-acct Equity:OpeningClosing:2001 \ Assets Liabilities > export /2001-opening.journal

👆 Assets Liabilities 是默认会带到 closing 或 opening 的 accounts,可以指定任何 accounts。

生成 2000 年的 closing journal 和 2001 年的 opening journal:

export/2000-closing.journal 1 2 3 4 5 2000-12-31 closing balances ; clopen:2001 Assets:Cash -48.90 CNY = 0.00 CNY Assets:Checking:ICBC -2,913.60 CNY = 0.00 CNY Assets:Deposit:Fixed -11,000.00 CNY = 0.00 CNY Equity:OpeningClosing:2001

export/2001-opening.journal 1 2 3 4 5 2001-01-01 opening balances ; clopen:2001 Assets:Cash 48.90 CNY = 48.90 CNY Assets:Checking:ICBC 2,913.60 CNY = 2,913.60 CNY Assets:Deposit:Fixed 11,000.00 CNY = 11,000.00 CNY Equity:OpeningClosing:2001

在 2001.journal 开头 include 其 opening journal:

2001.journal 1 2 3 4 5 6 7 8 9 include share/commodities.journal include export/2001-opening.journal ; Default year. Y2001 ; Default commodity. D 1,000.00 CNY ; transactions

可以创建一个文件,比如叫作 active.journal:

active.journal 1 2 include share/accounts.journal include 2001.journal

可以设定环境变量 LEDGER_FILE 的值为此文件的路径,那么执行 hledger 命令时就默认使用这个文件。

如果想把所有年份的 journal 放在一起处理,可以创建一个文件,比如 all.journal:

all.journal 1 2 3 4 5 6 7 8 include share/accounts.journal include 2000.journal include export/2000-closing.journal include 2001.journal include export/2001-closing.journal include 2002.journal ; ...

股票类交易记账 Track investments (2020) - hledger

主要的问题是多次买卖过程中的 存货估价法 。常见的方法有先进先出(FIFO)、后进先出(LIFO)、加权平均(Weighted Average Cost),参见 FIFO vs. LIFO vs Average Cost Method 。

考虑对于非高频交易使用 FIFO(加权平均要处理舍入误差)。每次买入都放进一个单独的 sub-account,以便追踪和核验。

例子:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 2013-01-28 买入 Assets:Investment:Silver:130128 100 XAGg @ 6.279 CNY Assets:Checking:ICBC -627.90 CNY 2013-01-29 买入 Assets:Investment:Silver:130129A 300 XAGg @ 6.197 CNY Assets:Checking:ICBC -1,859.10 CNY 2013-01-29 卖出 Assets:Checking:ICBC 1,862.40 CNY Expenses:Finance:CapitalLoss:Securities 4.90 CNY Assets:Investment:Silver:130128 -100 XAGg @ 6.279 CNY = 0 XAGg Assets:Investment:Silver:130129A -200 XAGg @ 6.197 CNY 2013-01-29 买入 Assets:Investment:Silver:130129B 500 XAGg @ 6.251 CNY Assets:Checking:ICBC -3,125.50 CNY 2013-01-30 卖出 Assets:Checking:ICBC 3,168.50 CNY Income:CapitalGain:Securities -48.40 CNY Assets:Investment:Silver:130129A -100 XAGg @ 6.197 CNY = 0 XAGg Assets:Investment:Silver:130129B -400 XAGg @ 6.251 CNY 2013-02-07 卖出 Assets:Checking:ICBC 635.00 CNY Income:CapitalGain:Securities -9.90 CNY Assets:Investment:Silver:130129B -100 XAGg @ 6.251 CNY = 0 XAGg ; 检查所有子账户都已经清零 Assets:Investment:Silver 0.00 CNY =* 0 XAGg

Caution

Balance assertion 的时候要带单位(如 = 0 XAGg)。只写 = 0 可能会被解读为 = 0.00 CNY(CNY 是默认币种),在此例中恒为真,失去了 assertion 应有的效果。

外币消费 基本原则:尽量保持 Expenses 账户的金额都是人民币。

兑换外币的时候,通过 @ UNITPRICE 记录 costs 。消费的时候,使用相同的 @ UNITPRICE,以便 hledger 可以自动计算出对应的人民币金额到 Expenses 账户上:

1 2 3 4 5 6 7 7/20 人民币换美元(100:679.08) Assets:CashExt 100 USD @ 6.7908 CNY Assets:Checking:ICBC -679.08 7/23 打车 Expenses:Traffic:Taxi Assets:CashExt -80 USD @ 6.7908 CNY

信用卡消费也一样,唯一的区别是 @ UNITPRICE 在还款的时候才确定。

如果再次兑换外币,可以与存量做加权平均,计算出新的平均 costs,避免管理先进先出:

1 2 3 4 5 6 7 8 8/10 人民币换美元(100:679.20) Assets:CashExt 100 USD @ 6.792 CNY Assets:Checking:ICBC -679.2 8/10 计算均价 Assets:CashExt 120 USD @ 6.7918 CNY Assets:CashExt -20 USD @ 6.7908 CNY Assets:CashExt -100 USD @ 6.792 CNY

通过 hledger print -x --infer-equity 查看的效果:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 2010-07-20 人民币换美元(100:679.08) Assets:CashExt 100 USD @ 6.7908 CNY equity:conversion:CNY-USD:USD -100 USD equity:conversion:CNY-USD:CNY 679.0800 CNY Assets:Checking:ICBC -679.08 CNY 2010-07-23 打车 Expenses:Traffic:Taxi 543.2640 CNY Assets:CashExt -80 USD @ 6.7908 CNY equity:conversion:CNY-USD:USD 80 USD equity:conversion:CNY-USD:CNY -543.2640 CNY 2010-08-10 人民币换美元(100:679.20) Assets:CashExt 100 USD @ 6.792 CNY equity:conversion:CNY-USD:USD -100 USD equity:conversion:CNY-USD:CNY 679.200 CNY Assets:Checking:ICBC -679.20 CNY 2010-08-10 计算均价 Assets:CashExt 120 USD @ 6.7918 CNY equity:conversion:CNY-USD:USD -120 USD equity:conversion:CNY-USD:CNY 815.0160 CNY Assets:CashExt -20 USD @ 6.7908 CNY equity:conversion:CNY-USD:USD 20 USD equity:conversion:CNY-USD:CNY -135.8160 CNY Assets:CashExt -100 USD @ 6.792 CNY equity:conversion:CNY-USD:USD 100 USD equity:conversion:CNY-USD:CNY -679.200 CNY

经由另一币种中转的外币消费 比如刷卡进行日元消费,但信用卡按美元记账,最后用人民币还款。希望可以记录下实际的日元金额、记账的美元金额以及对应的人民币金额。

方案一 简单的方式就是把日元仅当作「注释级事实」,不作为最终财务核算的信任来源:

1 2 3 4 5 6 7 8 2/1 饮料 Expenses:Catering:Drink ; 380 JPY Liabilities:Credit:ICBC -2.6 USD @ 7.2423 CNY 3/25 信用卡还款 Liabilities:Credit:ICBC 2.6 USD @ 7.2423 CNY == 0 USD Assets:Checking:ICBC -18.83

通过 hledger print -x --infer-equity 查看的效果:

1 2 3 4 5 6 7 8 9 10 11 2024-02-01 饮料 Expenses:Catering:Drink 18.82998 CNY ; 380 JPY Liabilities:Credit:ICBC -2.6 USD @ 7.2423 CNY equity:conversion:CNY-USD:USD 2.6 USD equity:conversion:CNY-USD:CNY -18.82998 CNY 2024-03-25 信用卡还款 Liabilities:Credit:ICBC 2.6 USD @ 7.2423 CNY == 0 USD equity:conversion:CNY-USD:USD -2.6 USD equity:conversion:CNY-USD:CNY 18.82998 CNY Assets:Checking:ICBC -18.83 CNY

其中 Assets 和 Liabilities 账户都可以对账,从而保证了 Expenses 的正确。

方案二 或者允许 Expenses 使用日元:

1 2 3 4 5 6 7 2/1 饮料 Expenses:Catering:Drink 380 JPY @@ 18.82998 CNY Liabilities:Credit:ICBC -2.6 USD @ 7.2423 CNY 3/25 信用卡还款 Liabilities:Credit:ICBC 2.6 USD @ 7.2423 CNY == 0 USD Assets:Checking:ICBC -18.83

日元上用 @@ TOTALPRICE 是因为此例刚好除不尽。

通过 hledger print -x --infer-equity 查看的效果:

1 2 3 4 5 6 7 8 9 10 11 12 13 2024-02-01 饮料 Expenses:Catering:Drink 380 JPY @@ 18.82998 CNY equity:conversion:CNY-JPY:JPY -380 JPY equity:conversion:CNY-JPY:CNY 18.82998 CNY Liabilities:Credit:ICBC -2.6 USD @ 7.2423 CNY equity:conversion:CNY-USD:USD 2.6 USD equity:conversion:CNY-USD:CNY -18.82998 CNY 2024-03-25 信用卡还款 Liabilities:Credit:ICBC 2.6 USD @ 7.2423 CNY == 0 USD equity:conversion:CNY-USD:USD -2.6 USD equity:conversion:CNY-USD:CNY 18.82998 CNY Assets:Checking:ICBC -18.83 CNY

借助 balance assertion 实现了 Expenses 在 costs 层面的校验。

最大的问题是在 Expenses 中引入了日元。

方案三 考虑引入中间账户作为美元到日元的过渡,叫 Equity:FX:Clearing。

不能叫 Equity:Conversion,会报错「Conversion postings must not have a cost」。

1 2 3 4 5 6 7 8 9 2/1 饮料 Expenses:Catering:Drink Equity:FX:Clearing -380 JPY @@ 18.82998 CNY Equity:FX:Clearing 2.6 USD @ 7.2423 CNY Liabilities:Credit:ICBC -2.6 USD @ 7.2423 CNY 3/25 信用卡还款 Liabilities:Credit:ICBC 2.6 USD @ 7.2423 CNY == 0 USD Assets:Checking:ICBC -18.83

这里有个问题是,如果日元的信息写错了,甚至对应的 @@ TOTALPRICE 错了,无法通过 balance assertion 实现校验。

Caution

hledger 的 balance assertion,

永远无法作用在「valuation / cost 折算结果」上。

可以通过 hledger bal Equity:FX:Clearing --cost 来检查其最终 cost amount 是否为零。如果不为零,通过 hledger reg Equity:FX:Clearing --cost 检查出错的位置。

方案四 事实拆分 + 人工一致性约束。把原本一条 transaction 的消费记录拆成两条:

银行事实(authoritative),USD → CNY 是锚点 商户事实(declarative),JPY 是锚点 1 2 3 4 5 6 7 8 9 10 11 2/1 饮料 [Bank] Equity:FX:Bridge 380 JPY @@ 18.82998 CNY Liabilities:Credit:ICBC -2.6 USD @ 7.2423 CNY 2/1 饮料 [Receipt] Expenses:Catering:Drink Equity:FX:Bridge -380 JPY @@ 18.82998 CNY == 0 JPY 3/25 信用卡还款 Liabilities:Credit:ICBC 2.6 USD @ 7.2423 CNY == 0 USD Assets:Checking:ICBC -18.83

通过 hledger print -x --infer-equity 查看的效果:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 2024-02-01 饮料 [Bank] Equity:FX:Bridge 380 JPY @@ 18.82998 CNY equity:conversion:CNY-JPY:JPY -380 JPY equity:conversion:CNY-JPY:CNY 18.82998 CNY Liabilities:Credit:ICBC -2.6 USD @ 7.2423 CNY equity:conversion:CNY-USD:USD 2.6 USD equity:conversion:CNY-USD:CNY -18.82998 CNY 2024-02-01 饮料 [Receipt] Expenses:Catering:Drink 18.82998 CNY Equity:FX:Bridge -380 JPY @@ 18.82998 CNY == 0 JPY equity:conversion:CNY-JPY:JPY 380 JPY equity:conversion:CNY-JPY:CNY -18.82998 CNY 2024-03-25 信用卡还款 Liabilities:Credit:ICBC 2.6 USD @ 7.2423 CNY == 0 USD equity:conversion:CNY-USD:USD -2.6 USD equity:conversion:CNY-USD:CNY 18.82998 CNY Assets:Checking:ICBC -18.83 CNY

和方案一其实没有本质区别了,而且也无法避免方案三中的问题。虽然对 Equity:FX:Bridge 账户的日元余额做了清零的校验,但无法校验两个 transactions 的汇率一致。就是说如果第二笔 transaction 的 @ UNITPRICE 或 @@ TOTALPRICE 写错了,balance assertion 不会报错,从而无法确保 Expenses 记录的人民币消耗是正确的。跟方案三类似,只能通过 hledger bal --cost 来检查。

个人记账的账户结构 Asset 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 Assets ; type: Asset ├─ Cash │ ├─ CNY │ └─ Foreign ; 可以开不同币种的子账户 ├─ Wallet ; e-wallets ├ ├─ Alipay ├ ├─ Paypal ├ └─ WeChat ├─ Checking ; 活期账户 │ └─ ICBC │ └─ Card1 ├─ Deposit ; 定期存款、存款类资产 │ ├─ CMB │ │ └─ Fixed1 ; 定期存款 │ ├─ ICBC │ │ └─ Large1 ; 大额存单 │ └─ Security ; 押金 │ └─ CounterParty1 ├─ StoredValue ; 3rd party merchant accounts (refundable) │ ├─ Huatai │ └─ TietaElec ├─ Prepaid ; 3rd party merchant accounts (not refundable) │ ├─ AppleStore │ └─ Linode ├─ Investment ; 投资类资产 │ ├─ CMB │ │ ├─ Jijin │ │ │ └─ Product1 │ │ ├─ Licai │ │ │ └─ Product1 │ │ └─ OtherProduct1 │ ├─ Huatai │ │ └─ Stock1 │ ├─ Alipay │ │ └─ YuEBao │ └─ WeChat │ └─ Licaitong ├─ Insurance ; 保险类资产 │ ├─ Gongjijin ; 公积金账户 │ ├─ Medical ; 医保个人账户 │ └─ PAIC │ └─ Product1 ├─ Lent ; 借出款项 │ ├─ Alice │ └─ Bob ├─ AccruedIncome ; 应收款项(比如公司欠发的工资) │ └─ Company1 │ └─ Salary ; Company1 欠发的工资 ├─ Reimbursable ; 可报销款项 │ └─ Company1 │ ├─ Conference │ └─ Traffic └─ Refundable ; 可退还款项 └─ Shop1

Liability 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 Liabilities ; type: Liability ├─ CreditCard ; 信用卡 │ └─ ICBC │ └─ Card1 ├─ Online ; Online credit accounts │ ├─ Huabei │ └─ Meituan ├─ Loan ; 贷款 │ ├─ ICBC │ │ └─ Installment ; 分期付款 │ ├─ CMB │ │ └─ PersonalCredit ; 个人信用贷 │ ├─ Car ; 车贷 │ │ └─ Car1 │ └─ House ; 房贷 │ └─ House1 ├─ Borrowed ; 借入款项 │ ├─ Alice │ └─ Bob ├─ Unpaid ; 未付账款 │ └─ Shop1 └─ Advance ; 预支款项 └─ Company1 └─ TeamBuilding

Revenue 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 Income ; type: Revenue ├─ Career │ ├─ Salary │ ├─ Overtime │ ├─ Bonus │ ├─ Allowance │ ├─ PartTime │ ├─ Subsidy │ └─ PreTax │ ├─ BasePay │ ├─ Allowance │ ├─ Bonus │ ├─ Award │ └─ StockRelated ├─ Finance │ ├─ Dividend ; 分红(含余额宝收益等) │ └─ Interest │ ├─ Bank ; 银行存款利息 │ ├─ Insurance ; 保险利息、红利 │ └─ Investment ; 非存款类理财产品的利息型收益 ├─ CapitalGain │ ├─ Property ; 房产等出售收益 │ └─ Securities ; 股票、基金、贵金属等出售收益 ├─ FX │ └─ Gain ; 外汇兑换收益 ├─ OperatingRevenue └─ NonOp ├─ Promotion ├─ RedPacket ├─ UsedGoods ; 二手物品出售 ├─ Windfall ; 意外之财 └─ Winning

Expense 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 Expenses ; type: Expense ├─ Appearance ; 形象(衣服饰品) │ ├─ Accessory │ ├─ Beauty │ └─ Clothing ├─ Catering ; 餐饮(食品酒水) │ ├─ Drink │ ├─ Material │ ├─ Meal │ └─ Snack ├─ Reside ; 安居(居家物业) │ ├─ Accommodation │ ├─ Cost │ ├─ Fitment │ ├─ Furniture │ └─ Rent ├─ Living ; 生活 │ ├─ Commodity │ ├─ Misc │ ├─ Service │ ├─ Software │ └─ Utilities ├─ Traffic ; 交通(交通出行) │ ├─ Airplane │ ├─ Gas │ ├─ Parking │ ├─ Public │ ├─ Rent │ ├─ Taxi │ ├─ Toll │ └─ Train ├─ Communication ; 交流通讯 │ ├─ Mobile │ ├─ Network │ ├─ Post │ └─ Telephone ├─ Entertainment ; 娱乐(休闲娱乐) │ ├─ Digital │ ├─ Games │ ├─ Leisure │ ├─ Party │ ├─ Pet │ ├─ Sport │ ├─ Toy │ └─ Travel ├─ Learning ; 学识(学习进修) │ ├─ Book │ ├─ Exam │ ├─ Training │ ├─ Tuition │ └─ Utilities ├─ Social ; 人情(人情往来) │ ├─ Charity │ ├─ Compensation │ ├─ Filial │ ├─ Gift │ └─ Treat ├─ Health ; 健康(医疗保健) │ ├─ Drug │ ├─ Equipment │ ├─ Examination │ ├─ Nourishment │ └─ Treatment ├─ Finance ; 金融 │ ├─ CapitalLoss │ │ ├─ Property ; 房产等出售损失 │ │ └─ Securities ; 股票、基金、贵金属等出售损失 │ ├─ Commission ; 手续费 │ ├─ Insurance │ ├─ Interest │ │ └─ House │ ├─ Investment │ └─ Service ├─ FX │ └─ Loss ; 外汇兑换损失 ├─ Society ; 社会 │ ├─ Compensation │ ├─ Insurance │ ├─ Penalty │ └─ Tax │ ├─ Bonus │ ├─ House │ └─ Salary ├─ Adjustments │ ├─ Discount ; 折扣 │ ├─ Rebate ; 返利 │ ├─ Refund ; 退款 │ └─ Rounding ; 四舍五入误差 ├─ Car ; 汽车 │ ├─ Accessory │ ├─ Insurance │ ├─ Maintenance │ └─ Utility └─ Misc ; 其他杂项 ├─ BadDebt ; 坏账损失(借出款项无法收回) ├─ Correction ; 账记错了 ├─ Fraction ; 零头金额处理 ├─ IncomeReversal ; 收入冲销 └─ Lost ; 丢失

Equity 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 Equity ; type: Equity ├─ Property │ ├─ Car │ │ └─ Car1 │ └─ House │ └─ House1 ├─ Society │ └─ Insurance │ ├─ Housing │ │ ├─ Employee │ │ └─ Employer │ ├─ Maternity │ │ └─ Employer │ ├─ Medical │ │ ├─ Employee │ │ └─ Employer │ ├─ Pension │ │ ├─ Employee │ │ └─ Employer │ ├─ Unemployment │ │ ├─ Employee │ │ └─ Employer │ └─ WorkInjury │ └─ Employer ├─ Household │ └─ Spouse ├─ Relatives │ ├─ Self │ │ ├─ Extended │ │ └─ Parents │ └─ Spouse │ ├─ Extended │ └─ Parents ├─ Social │ └─ EventGifts ; 特殊活动收受的礼金 ├─ Employer │ └─ Company1 ├─ Extraordinary │ └─ DebtForgiven ; 债务豁免 └─ OpeningClosing └─ 2026